2025 Q1: When the Market Gives You Lemons

05/09/2025

SEVEN STRATEGIES FOR NAVIGATING A DOWN MARKET

With the markets experiencing sharp declines this year, it’s no surprise that many investors are feeling uneasy. But while downturns can be unsettling, they can also open the door to some valuable financial

planning opportunities. Here are seven thoughtful strategies that may help you make the most of a down market.

1. PUT IDLE CASH TO WORK

Holding on to too much cash can quietly erode your wealth—especially when inflation and taxes eat into any potential gains. Over time, the stock market has historically outpaced inflation, making it an essential tool for long-term growth. If you’ve been sitting on extra cash, a market dip may be the perfect time to put those dollars to work. Think of it as buying quality investments on sale. Consider easing into the market through dollar-cost averaging to help smooth the ride. Yes, investing during volatility can feel daunting—but many investors regret missing out once the market recovers. Why wait to buy later at higher prices when you could take advantage of today’s discounts?

2. HARVEST TAX LOSSES STRATEGICALLY

Tax-loss harvesting isn’t just for year-end. If your portfolio has taken a hit, it may be a smart time to lock in those losses and offset gains elsewhere. One option? A tax swap between similar mutual funds or ETFs—selling one and purchasing another with a different structure to maintain market exposure. Just be sure the investments aren’t considered “substantially identical,” or you risk triggering the wash-sale rule. Consult a tax professional to ensure the strategy suits your specific situation. And if you’re curious about the rules, IRS Publication 550 is a great resource.

3. CONSIDER A ROTH CONVERSION

If your traditional IRA has taken a dip, you may want to explore converting it to a Roth IRA. A lower account value now means a potentially smaller tax bill on the conversion—and more room for tax-free growth in the future.

Why consider converting?

- No required minimum distributions (RMDs)

- Tax-free withdrawals if requirements are met

- A more tax-efficient inheritance for loved ones

- Greater flexibility for future tax planning

As always, weigh the benefits against your personal tax and financial picture before making a move.

4. GIFT TO FAMILY MEMBERS WHILE VALUES ARE LOWER

Thinking of making financial gifts to children or other family members? Now might be the right time. Gifting while asset values are down allows you to transfer those assets at a lower value—potentially reducing future estate taxes and giving those assets room to grow in your loved ones’ hands. It’s a thoughtful way to share your wealth and plan for future generations, all while navigating current market conditions.

5. USE IRA FUNDS FOR CHARITABLE GIVING

If you’re over 70½ and charitably inclined, consider using your IRA for donations. Qualified charitable distributions (QCDs) from an IRA can satisfy required minimum distributions (RMDs) and may reduce your taxable income. With many taxable accounts down, using IRA assets for giving can be more tax-efficient than selling appreciated securities or drawing from fallen accounts. Just make sure your donation is made directly from the IRA to a qualified charity.

6. CONVERT UGMA/UTMA ASSETS TO A 529 PLAN

Many families hold custodial accounts (UGMA/UTMA) for education savings—but these may be subject to the kiddie tax and count more heavily against financial aid eligibility. If those funds are intended for college, consider liquidating while values are down and transferring the proceeds into a 529 plan. A 529 offers tax-free growth and taxfree withdrawals for qualified education expenses—and is treated more favorably for financial aid purposes.

7. RESET THE COST BASIS OF COMPANY STOCK IN YOUR RETIREMENT PLAN

If you hold company stock in your retirement plan, you may already be familiar with the Net Unrealized Appreciation (NUA) strategy, which allows for long-term capital gains treatment when distributing shares. But what if your company stock has dropped in value? It might be worth resetting the cost basis by selling and then repurchasing the shares within the retirement plan—since the wash-sale rule doesn’t apply in this case. This “Net Unrealized Depreciation” strategy can potentially enhance the future benefit of NUA treatment. It’s a nuanced move, so definitely consult your financial advisor for personalized guidance.

WHEN MARKETS GET TOUGH, GET STRATEGIC

We can’t control the markets, but we can choose how we respond to them. While not every strategy here will be the right fit for you, each offers a potential silver lining in uncertain times. And remember—smart planning is always a good idea, no matter what the market is doing.

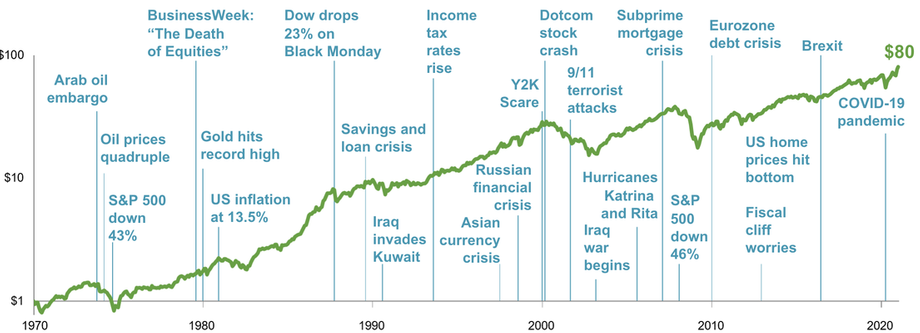

Markets Have Rewarded Discipline

Growth of a dollar - MSCI World Index (net dividends), 1970-2024

In US dollars. MSCI data © MSCI 2021, all rights reserved. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is no guarantee of future results.

TALK TO YOUR OWEN LEGACY GROUP ADVISOR

Before making any major financial decisions, connect with your financial advisor who understands your personal goals and tax situation. A customized plan can help turn today’s challenges into tomorrow’s opportunities.