First Quarter 2020 Investment Letter

2020 Q1 Edition

We are living through an extraordinary period in history that none of us will ever forget. The impact on our families, communities, and country has been profound. While several weeks ago we had reason for cautious optimism that the coronavirus might be largely contained to China, it is now obvious that is not the case. The United States and world are now facing the dual threats of a health crisis and an economic crisis. Both need to be fought with monumental government policy responses and individual behavioral changes.

We’ve frequently said that recessions and bear markets are inevitable phases within recurring economic and financial market cycles. We’ve also said there is always the risk of an unexpected “external shock” to the markets and economy (e.g., a geopolitical conflict or natural disaster). Investors need to be prepared for both to happen, but their precise timing is consistently unpredictable.

It’s one thing to say it and another to actually live it. But we will get through this crisis period. Things will improve and recover. Most importantly, we sincerely hope you and yours are able to remain healthy and manage well through this challenging period.

First Quarter 2020 Market Update

The first quarter of 2020 has proven to be unprecedented for financial markets. U.S. stocks fell into a 20% bear market in the shortest time ever. They continued to drop and declined 30% in a record 30 days! Volatility, as measured by the VIX, reached its all-time high on March 16. Oil’s 25% drop on March 9 was its biggest one-day drop since the 1991 Gulf War. Finally, 10-year and 30-year Treasury bond yields fell to all-time lows of 0.54% and 0.99%, respectively.

As of the market close on March 27, larger-cap U.S. stocks have fallen 21% year to date, having rebounded a bit from their historic drop. Smaller-cap U.S. stocks have done even worse, falling 32%. Foreign stocks have also suffered significant drawdowns, as developed international stocks have fallen 25% and emerging-market stocks have dropped 26%.

In the fixed-income markets, core bonds have gained 3%, once again playing their key role as portfolio ballast against sharp, shorter-term stock market declines. The 10-year Treasury yield is currently at 0.72%, down from 1.92% at year-end. In contrast, higher-risk floating-rate loans and high-yield bonds have suffered outsized losses, both dropping over 14%. Investment-grade corporate bonds have been far from immune, losing over 5%.

Uupdate on the Macro Outlook

We entered the year with an outlook for a moderate rebound in the global economy (especially outside the United States) on the back of reduced U.S.-China trade tensions and extensive global central bank monetary accommodation. Our base case now is that the U.S. economy is headed into recession in the second quarter. It is likely to be a severe one, with a sharp contraction in GDP and an unprecedented rise in unemployment.

The near-term economic damage from the United States’ and other countries’ response to the virus now looks almost certain to be severe (barring some unexpected major medical breakthrough in the near future). While we do not forecast economic data, the current Wall Street consensus first quarter and second quarter GDP forecasts are for annualized declines in the range of 12% to 30%.

The depth and duration of the recession—and the strength and timing of the ensuing recovery—depend on two key variables:

1. The effectiveness of our medical response and social policy efforts in flattening the curve

2. The speed and effectiveness of our fiscal, monetary, and regulatory policy response

One lesson learned from the 2008 global financial crisis is that a policy response needs to be significant and executed quickly. Governments need to make a credible commitment to “do whatever it takes” to support the economy and prevent a negative spiral from taking hold. As of this writing, the Federal Reserve and other major central banks seem to have gone all-in to support the fluid functioning of credit, lending, and financial markets, and their critical role as the “plumbing” of the real economy. Congressional Republicans, Democrats, and the Trump administration all seem to be in agreement that something substantial needs to be done and done quickly. On March 27, Congress passed, and the president signed into law, a $2 trillion stimulus package. (See information included for more information on stimulus specifics.)

Portfolio Positioning

When you diversify across asset classes and consider a variety of potential scenarios, there will always be leaders and laggards in your portfolio. Some positions, like U.S. stocks, work well in strong up environments like we experienced last decade, while we have incorporated others that benefit portfolios during tougher times like the start to the 2020s. Put together, they build resiliency and protect a portfolio from betting on a single outcome, which can be a disastrous financial result if the opposite happens.

After strong performance across all markets in 2019, we rebalanced portfolios in early 2020 to reposition portfolios at their target allocations. Along with this, we also made the determination to reduce high yield and floating rate funds and opted for increased core bond exposure. Our portfolio allocation to core fixed-income performed well as stock markets sold off, delivering strong absolute returns and significantly outperforming U.S. stocks. This allocation helped to offset some of the decline in stocks and should continue to do so if the selloff continues.

Following the U.S. stock market’s 20% decline in mid-March, we continue to assess the point at which we would consider rebalancing again to add back equities with better valuations.

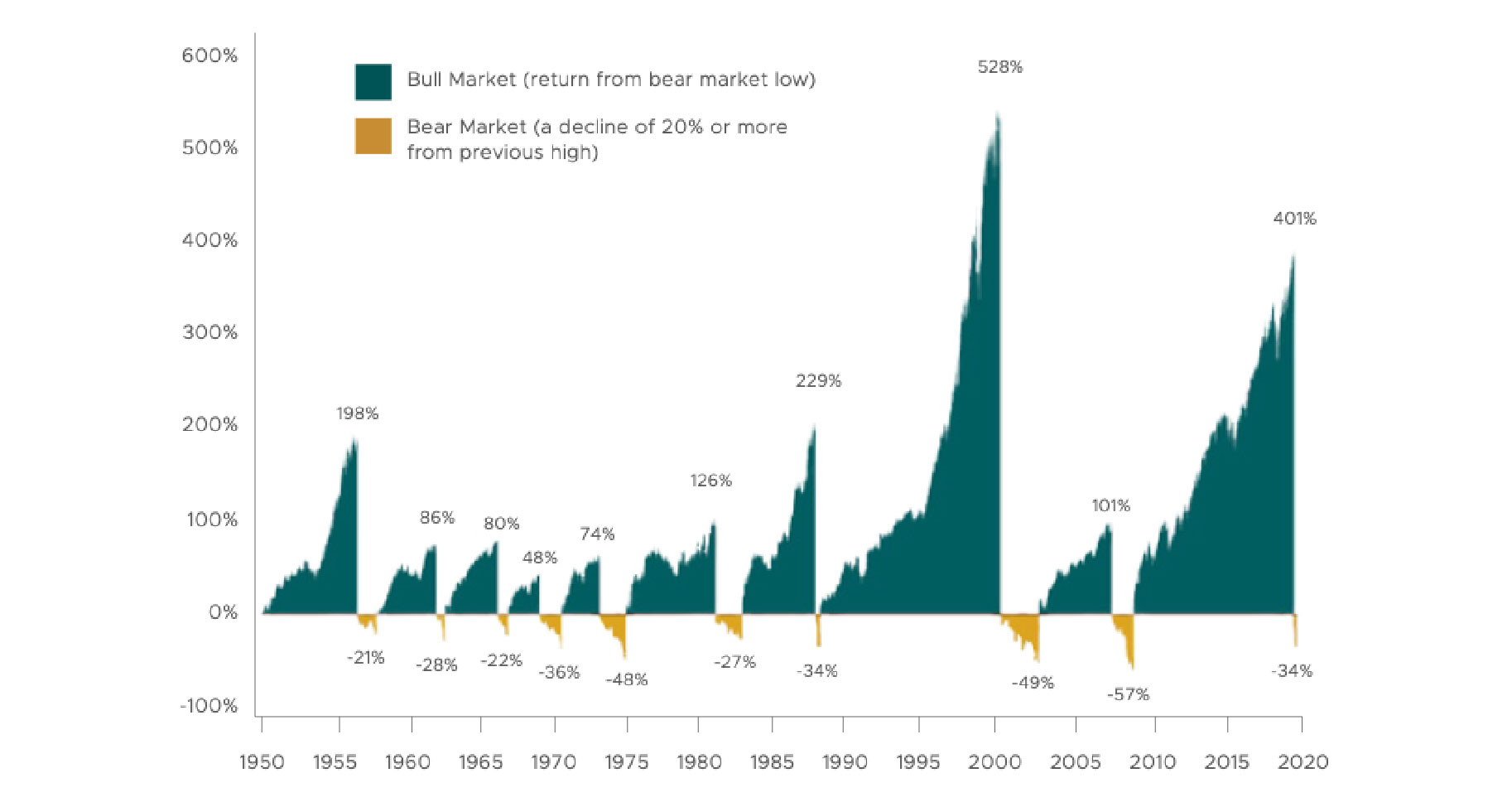

FIGURE 1 | Bull and Bear Markets: Putting Even Extreme Declines Into Perspective

© 2020. Litman Gregory Analytics, LLC. Source: Morningstar Direct. As of 3/23/20

However, given the still-negative trajectory of the virus in the United States, we have increased the margin of safety we want to see before doing so. Depending on S&P price levels, our base- case five-year expected return for U.S. stocks would be in the 9% to 12% range, annualized. A return in that range is in line or somewhat better than the long-term average for U.S. stocks. We believe that is sufficient compensation to justify a full or neutral allocation to equities overall. If there are additional market declines and valuations become even more attractive, we plan to increase our equity allocation to an overweight once stocks offer the likelihood of above-average returns.

Closing Thoughts

During these historic times, it is paramount to stay disciplined and recognize when emotion rears its head in investment decision making. If we invest based on emotion, we are very likely to exit the market after it has already dropped, meaningfully locking in losses. By the time the discomfort and worry are gone the market will already be much higher. That is not a recipe for long-term investment success.

Global markets have endured severe challenges and economic downturns in the past and have always weathered the storm. Attempting to time the market’s tops and bottoms is a fool’s errand. However, incrementally adjusting portfolio allocations in response to changes in asset class valuations, expected returns, and risks can be highly rewarding to long-term investors.

The time to be adding to stocks and other long-term growth assets is when prices are low and markets—and most of us personally—are gripped by fear and uncertainty rather than complacency, optimism, or greed. It may seem like the market could just keep dropping with no bottom in sight. But that is exactly where research, analysis, patience, experience, and having a disciplined investment process come most into play.

The precipitating event for the recent volatility is something none of us have experienced before: a global pandemic and an extreme societal response. One in two Americans now live under lockdown (and maybe more by the time you read this). Our medical infrastructure could be overwhelmed. We are probably already in a global recession. Facing this dual medical and economic crisis, the situation is probably likely to get worse before it gets better. We would love to be wrong. But it will get better.

The future is uncertain but our investment playbook remains the same: diversify; balance long- term returns with short-term risks; buy low into fear, sell high into greed. Stay the course.

– The Owen Legacy Group

The Market Commentary & Portfolio Strategy is mailed quarterly to our clients and friends to share some of our more interesting views. Certain material in this work is proprietary to and copyrighted by Litman/Gregory Analytics and is used by Owen Legacy Group with permission. Reproduction or distribution of this material is prohibited and all rights are reserved.