Retirement Through the Ages: 20-70

The word “retirement” means something different to everyone and often changes as we move through each stage of our lives. We go from our 20s where we almost cannot fathom retiring, to our 40s where our lives are so busy we wish retirement were tomorrow, and into our 60s, where suddenly it has become a reality. The statement, “I AM going to retire” could spark feelings of jubilation, trepidation or anything in- between. Regardless of what retirement means to you, here are a few thoughts and helpful questions to ask yourself at each step along the way.

In Your 20s: Establish Good Financial Habits

Your 20s are a time of self-discovery: You try out different career paths, life trends and cities to live in. This is a time when many of us have limited disposable income. Top of mind is typically how we are going to pay rent, not fund our retirement.

However, your 20s are a very important time to establish good habits that will set you up for a successful path to retirement. Ask yourself:

1. Have I opened a retirement account? If your employer offers a 401(k), start there. Set yourself up with an automatic paycheck deferral to make your contributions. If you are wondering whether you should make Roth or traditional contributions or which investments to choose, call your Owen Legacy Group (OLG) advisor and we will walk you through your options to determine what is right for you. If your employer does not offer a retirement plan, let us help you determine which retirement account options are available to you. When it comes to saving for your retirement in your 20s, the most important thing to do is to start. Once you have established your account and are making monthly contributions, you can go back to life as usual, and be pleasantly surprised at the end of each year as you see your retirement assets grow.

2. Have I left my 401(k) behind? You may have multiple jobs in your 20s while you search for a career that fits you best. Make sure you do not leave your 401(k) behind when you leave your employer. Talk to your OLG advisor about consolidating your retirement accounts when you leave employment to minimize the possibility of forgetting about money you have so dutifully saved.

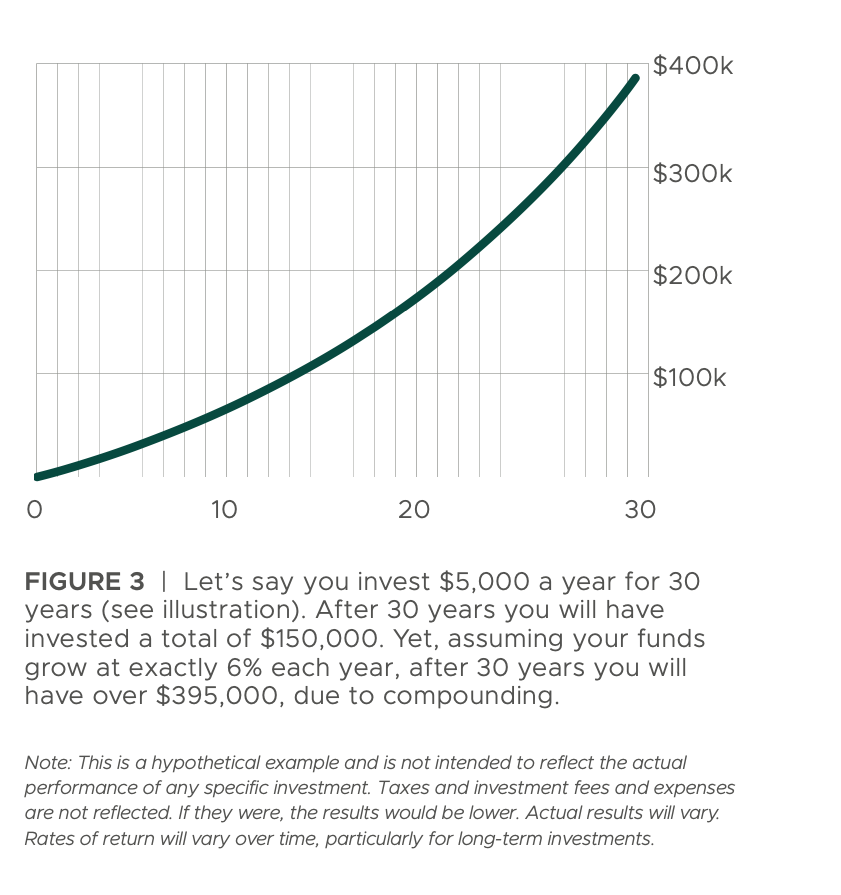

3. Do I understand the benefit of compounding interest? Compounding interest is a powerful tool on your side as you get started. Don’t worry about the ups and downs of the market—you have a long time until you are going to use that money, so let it grow and reap the benefits of volatility, time and compounding. These benefits can be clearly seen in the below illustration:

Compounding has a “snowball” effect. The more money that is added to the account, the greater its benefit. Also, the more frequently interest is compounded—for example, monthly instead of annually—the more quickly your savings build. The sooner you start saving or investing, the more time and potential your investments have for growth. In effect, compounding helps you provide for your financial future by doing some of the work for you.

In Your 30s: Increase Your Savings Not Your Spending

1. Have I increased my deferral amount as my income has increased? You are probably thinking: “There is no way I could increase the amount I am deferring to my retirement account. I have a new baby, a mortgage and I would really like a new car.” However, this is the time to make sure that as your income slowly increases, so does the amount you are saving. It is easy to allow your lifestyle to creep upwards, so challenge yourself to increase your deferral amount by 1% of your earnings each year.

2. Do I want to retire early? If you do, ask yourself the questions listed for ages 40-70.

3. Does my employer offer any other retirement benefits? Your employer may offer other benefits that you are not taking advantage of. Bring in your benefits package for review either with your HR department or with your OLG advisor. We can help make sure you understand and are taking advantage of all that your employer is offering.

In Your 40s: Start to Define Your Vision of Retirement

In your 40s, have an honest conversation with yourself about what you want retirement to look like. Appropriate questions to consider are:

1. Do I want to retire early?

2. How much should I have saved to feel confident about retiring?

3. What is holding me back from the retirement I have always wanted?

4. Where do I want to retire?

5. What could really throw my retirement plan off track?

6. Am I going to have to support anyone else in my retirement, such as children or parents?

7. What do I want to do with my time when I am retired?

If you are having a difficult time answering these questions, use this as an opportunity to have a retirement planning meeting with your OLG advisor. We can help you place a monetary framework around your hopes and dreams while also helping to spur conversation and imagination. You still have time before you are going to retire, so don’t worry if you can’t answer these questions yet.

In Your 50s: It's Time to Plan in More Detail

1. Do I have a retirement plan? This is a great time to come in and start the formal retirement planning process. For most people, there is still time to plan and save, but you now have the advantage of more clarity about what is right for you. We can help you plan and monitor your progress along the way.

2. Am I comfortable with how my retirement is invested? Start to look more closely and more frequently at your asset allocation as you near your retirement date. You do not necessarily have to be more conservative as you get older, but you do want to ensure you are very comfortable with your risk profile as you near retirement.

3. Are my savings on track? Your 50s are a great time to make up for shortfalls in your retirement savings. For many people, these will be their top earning years, making it easier to increase your savings in both retirement and non-retirement accounts.

At this point, you may be able to save more than the maximum deferral to your retirement account. This does not mean you should spend the rest; rather, save it outside of a retirement account. You want to have a balance between your retirement and non-retirement assets.

In Your 60s: Put Your Plan Into Action

1. Do I have a distribution plan that includes all of my income streams? As you get closer to retirement, you will want to determine how you are going to replace your monthly income. We will want to look at all income sources: Social Security, rentals, pension, retirement accounts, savings, etc., to determine the most efficient way to meet your monthly spending needs.

2. When am I going to take Social Security? Most people receive Social Security, and we want to ensure you have thought about when you would like to start.

3. Have I signed up for Medicare? The cost of health insurance continues to rise and for most, switching to Medicare saves you money. But it does not happen automatically, so mark your calendar for three months before you turn 65 and make sure you sign up.

In Your 70s: Make the Decision That is Right for You

Many people decide that the traditional age of 65 for retiring is not right for them. You may be one of the lucky ones who truly loves what you do and could not imagine going a day without your job. Others retire from their career only to find their next passion in another career. Hopefully at this point you have done the hard work of saving and are able to enjoy every day exactly as you envisioned.